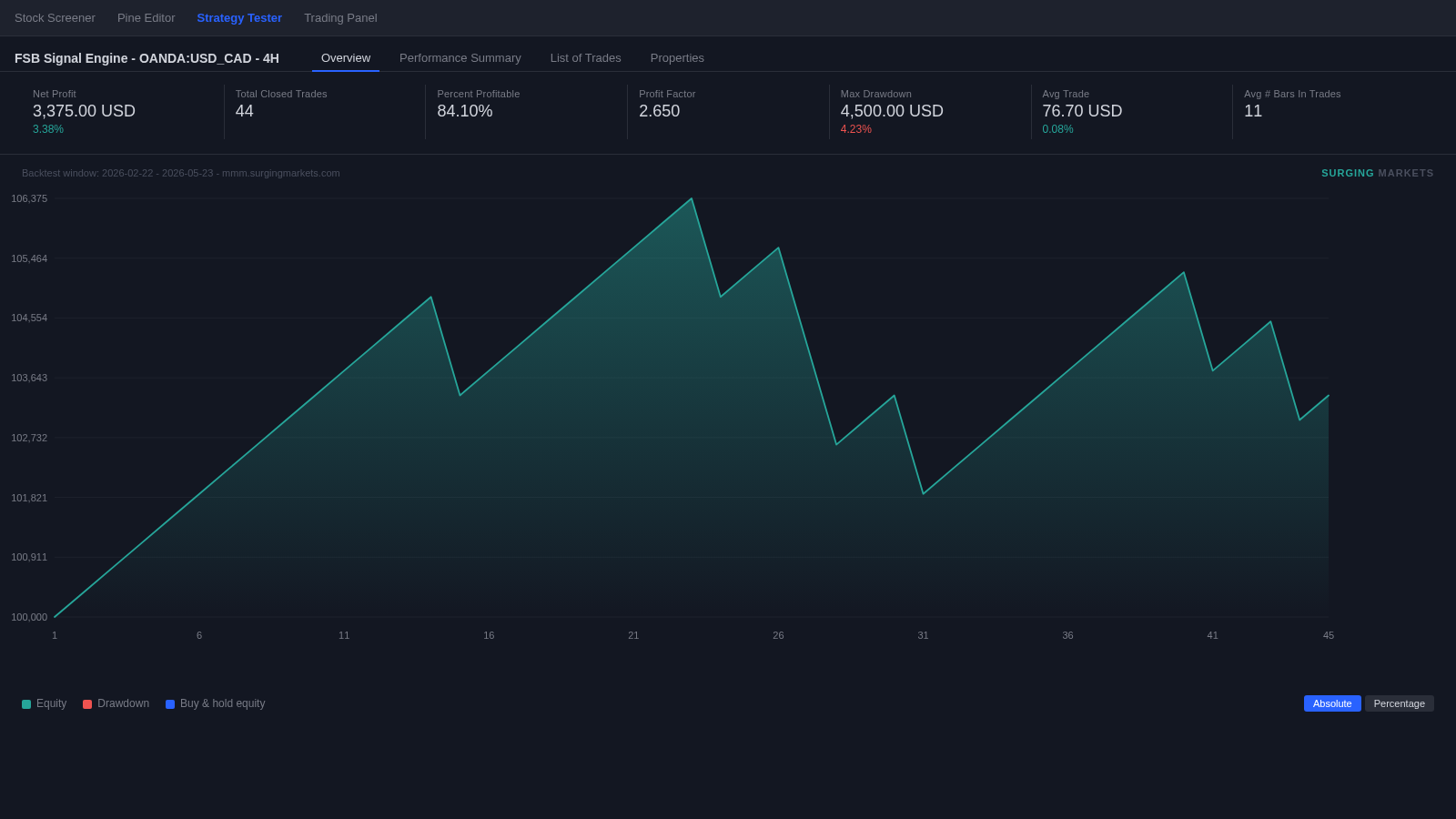

USD/CAD

4H

84.1%

Win Rate

Total Trades

44

Profit Factor

2.65

Net R

+2.24R

Max DD

2.00R

2026-02-21 → 2026-05-23

· 37W / 7L

Live on chart →

Typical results: Backtest only. Results not typical of subscribers. Past performance is not indicative of future results. Trading involves substantial risk of loss. Methodology.